ABOUT C.C.S. SERVICES

What a registered Credit Cooperative Society does -

The Credit cooperative societies are playing a vital role in India’s financial ecosystem by serving the credit needs of their members, who are often from economically weaker sections of the state. These societies operate under the cooperative Act and Rules of the local government. The cooperative societies based on the principles of voluntary membership, democratic governance, and mutual assistance.

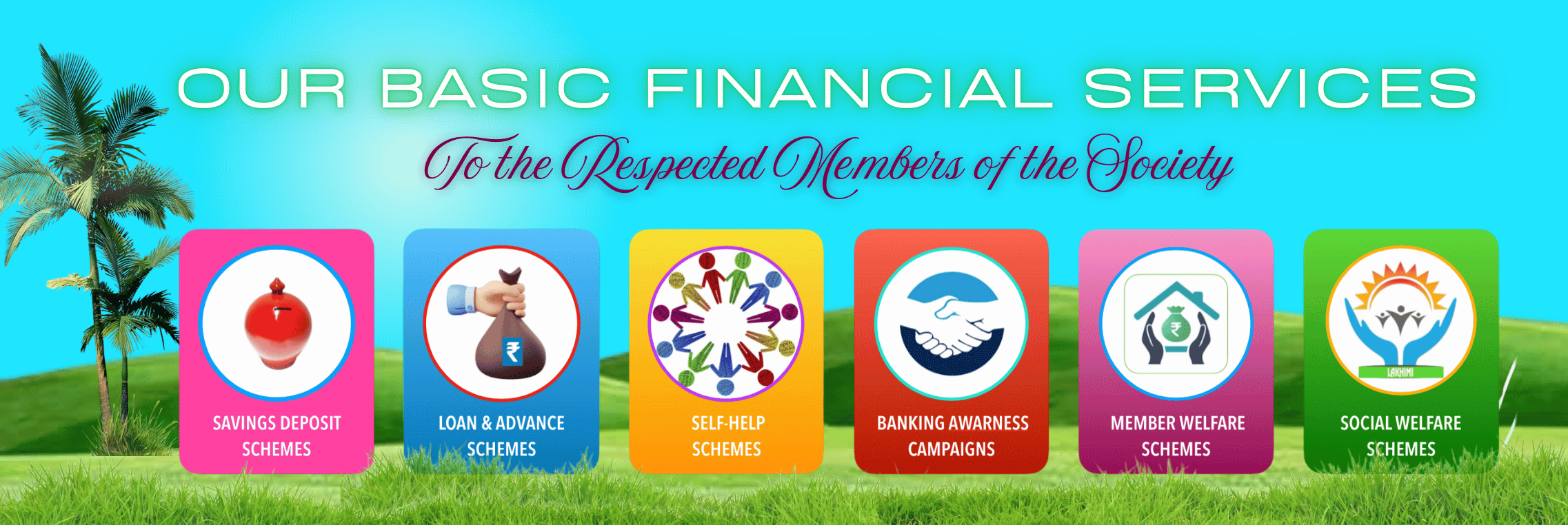

1. Savings and Deposits : Credit cooperative societies encourage their members to save money by offering various savings schemes, such as regular savings accounts, fixed deposits, and recurring deposit schemes. Members earn interest on these deposits, thus promoting the habit of saving.

2. Providing Credit : One of the primary functions of credit cooperatives is to provide loans to their members. These loans can be for personal needs, education, housing, agriculture, and business development. The interest rates on these loans are comparatively lower than those offered by traditional banks, making credit more accessible by easier processing, minimal documentation and affordable interest rates to the members.

3. Promoting Financial Inclusion : Credit cooperative societies play a significant role in promoting financial inclusion among underserved populations, including farmers, small business owners, and low-income individuals. They provide essential financial services to those who may not have access to mainstream banking system due to various barriers. Till this date we’re having on 2025 still there are various barriers presence in the society towards socio- economic development, where we are focusing, such as below :

- Lack of Financial Knowledge : Many individuals, particularly in rural areas, may not possess adequate financial literacy to navigate traditional banking services. Credit cooperative societies help bridge this gap by offering education and guidance, empowering members to make informed financial decisions.

- Banking Awareness : Credit cooperatives actively promote awareness of banking services, ensuring that members understand the products available to them. By organising workshops, seminars, and community meetings, these societies educate members about savings, loans, and other financial products.

- Affordability : Traditional banking institutions often impose high fees or interest rates, making financial services inaccessible to low-income individuals. Credit cooperative societies typically offer lower interest rates and nominal fees, which makes borrowing more affordable for their members.

- Geographic Accessibility : Many individuals live in remote or rural areas, where access to conventional banks may be limited. Credit cooperative societies operate locally, bringing financial services closer to these communities. This localised approach facilitates easy access for members who may otherwise face significant travel barriers.

- Tailored Financial Products : Understanding the unique needs of their members, credit cooperatives design specialised financial products and services that cater specifically to low-income individuals and small businesses. This includes micro loans, agriculture loans, and flexible repayment options that align with the income cycles of farmers and entrepreneurs.

- Building Trust : Due to their community-oriented nature, credit cooperatives foster trust among members. They are often managed by locals who understand the needs and challenges of the community. This trust encourages individuals who may be wary of traditional banks to engage with financial services.

- Supporting Entrepreneurs : For small business owners, credit cooperative societies offer invaluable support by providing the necessary capital to start or expand their enterprises. This financial backing enables them to contribute to local economies and create jobs within their communities.

By addressing these barriers and actively working to include marginalised groups in the financial system, credit cooperative societies are pivotal in enhancing financial inclusion in India. They empower individuals, promote selfsufficiency, and contribute to overall economic development and stability within their communities.

4. Cooperative Principles : Operations are governed by the principles of mutual assistance and democratic governance. Members have a say in decision-making processes, which fosters a sense of ownership and community.

5. Financial Education and Counselling : Many credit cooperatives engage in educating their members about financial literacy, budgeting, savings, and responsible borrowing. This empowerment helps members make informed financial decisions.

6. Insurance Services : Some credit cooperative societies also offer insurance products, including life insurance and health insurance, to safeguard their members’ financial well-being in times of need.

7. Investment Opportunities : Offering members various investment options, such as mutual funds or other financial instruments, to help grow their savings.

8. Capacity Building : Credit cooperatives often participate in capacity-building programs to enhance their operational efficiency and improve the financial literacy of their members. These initiatives foster sustainable growth and better service delivery.

9. Community Development : Beyond financial services, many credit cooperatives engage in community development activities, supporting local initiatives, infrastructure projects, and social welfare programs that benefit their members and the wider community.

10. Support for Agriculture and Rural Development : A significant portion of credit co-operatives focus on agricultural financing by providing necessary credit and resources to farmers, enabling them to invest in crops, livestock, and sustainable farming practices.

11. Regulatory Compliance : Credit cooperatives in India operate under the framework of the Cooperative Societies Act, ensuring compliance with regulations intended to protect the interests of members and maintain the integrity of the cooperative movement.

Credit cooperative societies in India serve as an essential mechanism for promoting economic self-reliance among communities, fostering financial stability, financial upliftment, update livelihood and enhancing the quality of life for their members.